Life is unpredictable, and financial surprises hardly come at the right time. A car accident, unforeseen medical expenses, or being fired can easily blow your budget out of proportion. That is where “What Is an Emergency Fund?” becomes a significant question for any person who aimed to establish financial safety.

An emergency fund is nothing more than a cash buffer that is meant to take care of emergencies that may be unplanned and urgent without necessarily having to use debt or borrowing. It is a very simple thing; however, once many people experience a certain crisis, they realize its significance.

We will get into the details of what it is, why it is important, and how much you ought to save in this article and how it works compared to regular savings. We will also discuss some real-life examples and various forms of emergency funds to enable you to construct one that suits your lifestyle.

What Is an Emergency Fund?

An emergency fund is a dedicated amount of money set aside specifically for unexpected financial emergencies. It is not to be used on vacation, on shopping, or on planned expenses, but rather on emergencies that you cannot foresee or evade.

To understand What Is an Emergency Fund?, think of it as your financial cushion. When you are faced with the need to cover a sudden stop in your income or you are faced with an emergency that requires you to cover it, then this fund assists you to remain afloat without having to borrow money at high interest rates.

Simply put, it serves as a shield between you and financial strains. Lack of it promotes even minor crises into long-term debts.

Why an Emergency Fund Matters

When you consider real-life situations, it becomes easier to understand what is an emergency fund and why it is important. Emergencies do not provide warnings, and prepared money may be the difference between stability and economic distress.

To illustrate, just consider losing a job out of the blue. In the absence of savings, you may not be able to afford rent, utility bills, or even groceries. An emergency fund is necessary so that even when you are unable to earn or recover, you can still afford the basic needs.

Peace of mind is another reason why it is important. One of the most common stressors is money problems, and the assurance that you have spare money to rely on when in need of it lowers anxiety levels in challenging situations. It also prevents high-interest debt such as credit cards or payday loans.

Surprisingly, in certain areas, individuals depend on government programs’ emergency funds in times of crisis like unemployment or disasters. Nevertheless, they are usually constrained, slow, or not promised, further emphasizing personal savings.

What Should be in an Emergency Fund?

One of the financial questions I have encountered often is “What is an emergency fund? How much should I have in it to be sure?” Although the exact figure will depend, the financial gurus usually suggest the saving of three to six months of basic living costs.

This covers rent, groceries, transport, utilities, and the basic bills—not the luxury bills. It might be prudent that those whose income is not stable (such as freelancers) should strive even higher.

It is not an aim to have a massive amount within a night but to grow over time. It can be as simple as a difference in small emergencies with a small buffer of $100 or even $500. The gradual build-up will eventually make it a stable financial cushion.

Emergency Fund vs Savings

It’s common to confuse an emergency fund with regular savings, but they serve different purposes. Understanding emergency funds vs. savings helps you manage money more effectively.

The savings are usually applied towards any planned purposes such as purchasing a car, going on vacation, or investing in education. These are foreseeable and can be timetabled.

An emergency fund, though, is only to be used in unforeseen emergencies. Accessibility and purpose are the major difference. Although savings can be invested or kept in accounts, emergency funds are best kept just in reach, typically in a savings account that has the facility of quick withdrawals.

Having them apart will help you not to use your safety net up accidentally on other non-emergency needs.

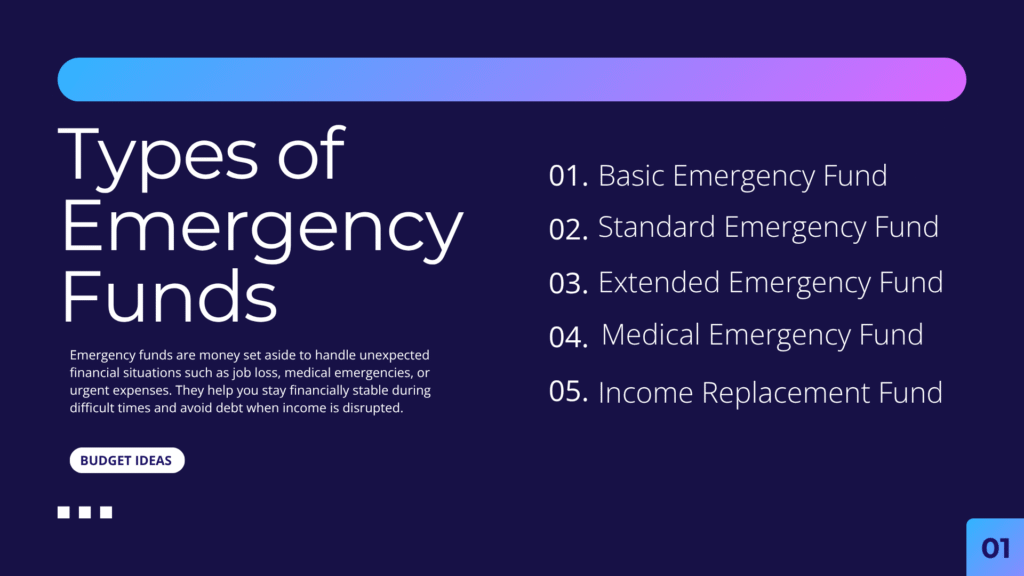

Types of Emergency Funds

There are different approaches when building financial safety nets, often referred to as types of emergency funds based on personal needs:

Basic Emergency Fund— Provides basic living needs during 1-3 months. Appropriate to students or low-income persons.

Normal Emergency Fund — Meets 3-6 months of expenditures. This is the most generally suggested level.

Extended Emergency Fund— Addresses 6-12 months of expenditure. Best suited to freelancers, business owners or individuals with fluctuating incomes.

Hybrid Emergency Fund— Integrates money market accounts with liquid investments such as cash savings to be flexible and grow.

Each type depends on income stability, lifestyle, and financial responsibilities.

Emergency Fund Examples

To have a clearer picture of how it works, we will consider a couple of emergency fund examples:

A wage earner deposits three months of rent, bills, and food in a different bank account. They invest this money to pay bills as they seek another job when their company is retrenching.

A freelancer saves inconsistent revenues when revenues are high. When their work is slowed down, the fund assists them in meeting minimum living standards.

A family maintains an independent account that is used in case of medical emergencies so that its hospital bills do not interfere with its monthly budget.

These examples show how an emergency fund acts as a financial shock absorber in real life.

Building Your Emergency Fund Step by Step

You do not need a lot of income to create an emergency fund. Consistency is the key. Begin with a modest goal each month—even 5% to 10% of your earnings. It can be simplified by automating the process of transfer to a separate account.

You can also accelerate your progress by cutting unnecessary costs, like unused subscriptions or impulse buying. Small donations accumulate over time to create a robust financial cushion.

Conclusion:

Understanding What Is an Emergency Fund? is one of the most important steps toward financial independence. It is not just money saved—it is protection against uncertainty, stress, and debt.

Whether you are starting small or building a long-term financial cushion, the key is consistency and discipline. Once established, it gives you confidence to face unexpected situations without panic or financial instability. In the end, having an emergency fund is not about how much you earn, but how well you prepare for the unexpected.

Leave A Comment