As your business grows or becomes more complex, it becomes essential to have a budget plan. Having a knowledge of budgeting helps you understand how much money you earn, how much money you spend, and where it goes each month. It becomes much easier to manage money when you have clear plan.

A budget is simply a plan for your money that outlines expected income and expenses over a specific period, typically a financial year. It tells your income where to go instead of you wondering where it went. This not only provides a clear view of your costs but also acts as a roadmap for managing and allocating financial resources to achieve your strategic goals.

To find financial peace, you need a system that works for you, not against you. In this article, we will explore why you need a strategy and break down four distinct types of budgets. These four budgeting methods each have their own advantages and disadvantages, which will be discussed in more detail below.

Why You Need a Budget (That Actually Fits):

Before moving forward, it is helpful to understand what a budget actually is. Budgeting is not about spending money; it is a clear and structured plan for your money. Choosing the right budgeting framework ensures that your financial planning aligns with your primary goals.

With a business budget in place, you can allocate resources such as funds, headcount, and materials precisely. It helps prioritize spending according to its importance and impact on business goals.

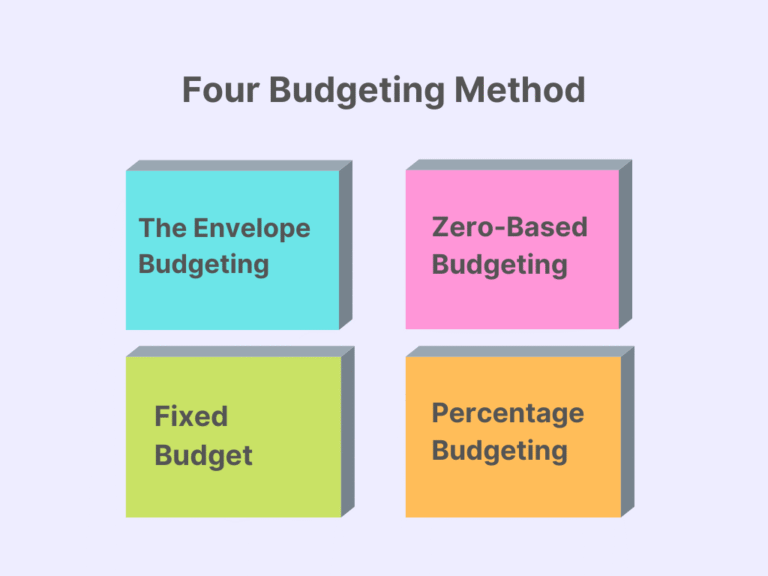

Types of Budgets:

Every budget is designed to serve a specific goal. Each type helps manage finances in a specific way depending upon needs and demands.

1. Zero-Based Budgeting: Give Every Dollar a Job

Zero-based budgeting (ZBB) is a strategic financial plan where each new financial period starts from zero. Managers must be able to justify every single expense, regardless of whether it was a part of the previous budget. No expenses are automatically “fixed”. It is a part of high accountability. Unlike traditional budgeting, which typically builds on previous budgets, ZBB involves reviewing and justifying every cost, focusing on strategic goals and financial performance.

The core philosophy is simple: Income minus Expenses (including savings) equals zero. This doesn’t mean you have zero dollars left in your bank account; it means you have zero dollars left unassigned. Every penny is accounted for before the month even begins.

Let’s discuss it with a simple example: if you earn $2000 a month and your bills and savings come out to $1,950, you aren’t finished. You must take that remaining $50 and assign it a job, such as “Car Repair Fund” or “Friday Night Pizza.”

Key Insights:

It prevents “lifestyle creep” because extra money is immediately categorized.

This budgeting method can reduce costs by preventing automatic increases from previous budgets.

Although Zero-based budgeting is time consuming, but it provides more detailed insights compared to traditional incremental budgeting.

While primarily used by businesses, it can also be beneficial for individuals and families.

By implementing Zero-Based budgeting, you know exactly where your money is going.

2. The Envelope Budget: Cash is King

The Envelope budgeting method is a practical budgeting method in which income is divided into specific expense categories, and a set amount is assigned to each category. It is a time-tested way to manage money. Traditionally, people divided their cash into separate envelopes for different expenses such as groceries, entertainment, and savings. Once the money in an envelope is used up, spending in that category stops until the next budget period, helping people stay aware of their limits.

In an increasingly digital world, sometimes the old ways are still the best. The Envelope Budget focuses on curbing variable spending. While you might pay your rent or mortgage online, you withdraw cash for categories that tend to fluctuate, like groceries, dining out, and entertainment.

There are modern twists on this, too. Several banking apps allow you to create digital “buckets” or sub-accounts that function just like envelopes, declining the transaction if the bucket is empty.

Key Insights:

All of your income is allocated to specific categories, resulting in a zero balance.

It motivates you to assign funds to specific goals, such as saving for emergencies, paying off debt, or investing. It aligns your spending with your overall financial goals.

This budgeting is especially effective for managing day-to-day expenses.

It is physically impossible to overdraft or go into debt while using the envelope budgeting method.

This budgeting method increases awareness of where money is being spent.

3. The Fixed (Static) Budget: Set It and Forget It

A fixed budget ( or static budget) is a budget plan that remains unchanged regardless of income fluctuations. It is a method of budgeting where you set a specific amount of money for each expense category at the beginning of the period and do not change it, no matter what happens.

For example, you decide to spend $300 on groceries and $200 on entertainment each month, and this amount will remain the same until the next budget cycle.

Fixed budgeting is often used by businesses to control overhead, but it is especially helpful for retirees or people with fixed expenses who want to make sure they never spend more than their baseline.

Key Insights:

It is highly predictable and requires very little maintenance once set up.

It is rigid. It doesn’t easily account for inflation, emergencies, or spontaneous life events, which can make it feel restrictive.

Fixed budgets set specific amounts for each expense category and do not change during the budget period.

4. The Percent-Based Budget (50/30/20 Rule)

Popularized by Senator Elizabeth Warren, the 50/30/20 rule divides your after-tax income into three broad buckets:

50% for Needs: Essential costs like housing, food, transportation, and utilities.

30% for Wants: Flexible spending like dining out, hobbies, and entertainment.

20% for Savings/Debt: Retirement contributions, emergency funds, and extra debt payments.

This is often the best starting point for beginners. It works well for those who want a balanced approach between enjoying life today and saving for tomorrow.

Key Insights:

It is flexible and easy to visualize. If your income goes up or down, the ratios scale with you effortlessly.

This budgeting method provides a clear and easy-to-follow method for managing money.

It is flexible enough to slightly adjust the percentage based on personal goals or circumstances and you don’t need to micromanage categories

How to Choose the Right Budget for You:

Choosing between these different types of budgets comes down to self-awareness. Ask yourself:

Do I find comfort in details or do they stress me out? (Details = Zero-based; Big Picture = 50/30/20)

Is my income stable or variable? (Stable = Fixed; Variable = Zero-based)

Do I struggle with impulse spending? (Impulse issues = Envelope system)

Remember, the “best” budget is simply the one you will actually use. A perfect spreadsheet that you never open is infinitely worse than a messy envelope system that keeps you out of debt.

Conclusion

Conclusion:

We’ve covered the four main pillars: the precision of Zero-based budgeting, the consistency of the Fixed budget, the flexibility of the Percentage-based method, and the discipline of the Envelope system.

Budgeting often gets a bad rap for being restrictive, but in reality, it’s about permission. It allows you to spend money without guilt, knowing that your bases are covered. By understanding the different types of budgets, you can choose a tool that empowers you rather than forces you.

Ready to take control? Pick one method from this list and commit to it for a 30-day trial period. Let us know in the comments below which method you are going to try first!

Leave A Comment